Hello @alexisdevelopments ,

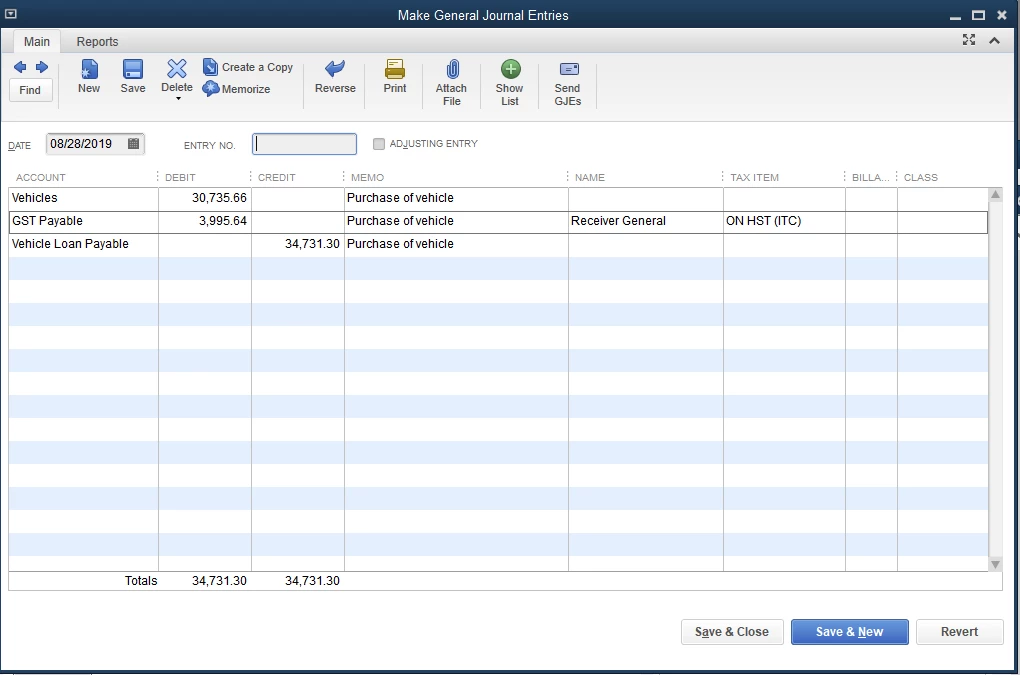

This is not a truck expense. It is a depreciating asset to your company, if you truly own it. Also, it depends on whether you are incorporated or not as to how you write off the associated truck expenses. If you are incorporated, you would make a JE for the truck purchase as follows (this is assuming a 13% HST tax is in play) :

Note that 1) The pre-tax cost of the vehicle is put to a Fixed Asset account, not an expense, 2) The loan needs to be set up as a Long Term Liability and 3) Interest is not a part of this initial transaction.

If your company is not incorporated but rather is a sole proprietorship, then you don't record any of this in your books. You take care of the vehicle expenses on the personal income tax return on form T2125 B1, so you still need to keep all your records for tax time. You would record the asset in the correct asset class (most likely Class 10 or 10.1) and only record the purchase price plus taxes. The interest is handled in another part of the form. You can only claim depreciation on the purchase price + taxes, not on the interest. Also good to note is that if you are a sole proprietor or partnership, you still must keep a vehicle log and you can only write off the percentage of expenses that pertain to your business kilometres driven, for example, fuel, maintenance, insurance costs, etc. These are not to be recorded in your books but only on this tax form at tax time.

Conversely, if the vehicle is owned by a corporation, you can record 100% of that vehicle's operating and maintenance costs, although if it is not being used 100% for business, then a calculation must be made to attribute a portion of those costs to you personally, thus reducing the business write off portion.

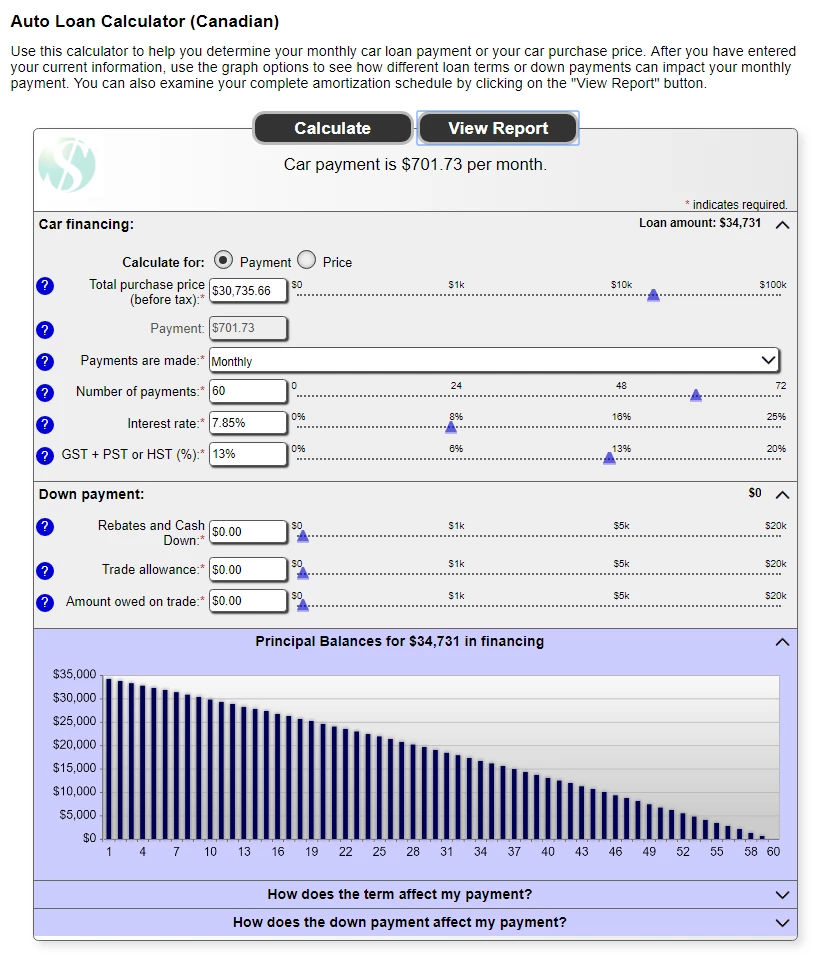

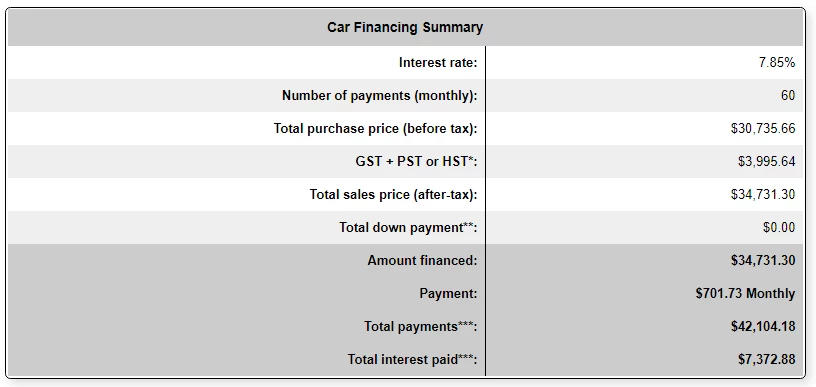

Carrying on with an incorporated company process subsequent to the purchase of the vehicle, you would then need to create an amortization list of your vehicle purchase. This is a good one. https://www.cchwebsites.com/content/calculators/CAAutoLoan.html.

Here is a sample (with me making a lot of assumptions . . . i.e. a 60 mo (5 yr) term, and a fudged interest rate to come as close to the interest amount as you have indicated.)

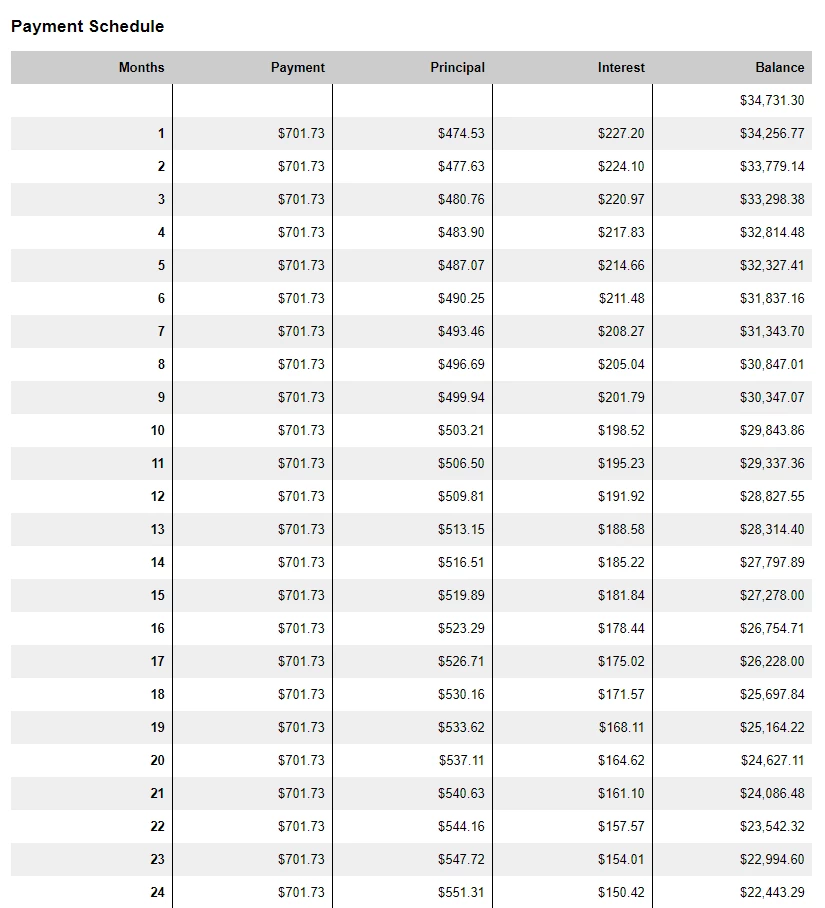

You would click on View or Print report to get the payment schedule. This is a very accurate calculator and if you input the correct numbers, you should come out to the exact same numbers as the bank.

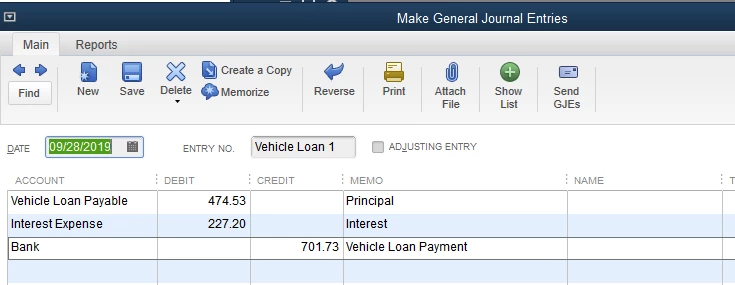

Now you set up a JE each time a payment is made to the bank and split it between principal and interest according to this schedule. In each journal entry you are going to decrease the amount of your loan, and increase an Interest expense account as follows: (this is assumed to be the first payment in this schedule)

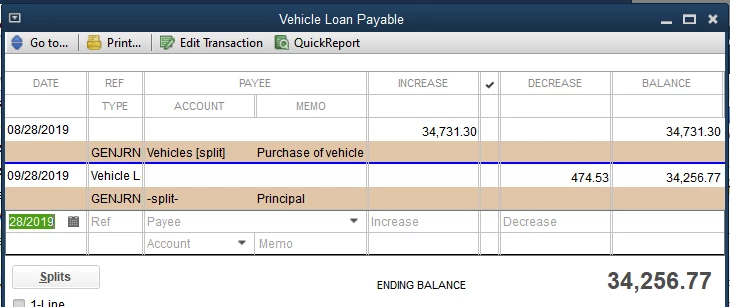

For each monthly payment you make, the principal and interest amount are going to change, with principal going up slightly each month and interest going down slightly. Note when you check your Vehicle Loan Payable register, the original loan amount is being reduced by the amount of the Principal payment only.

Interest is the only thing you can write off as an expense for each payment, which shows on the P & L.

If you have an external accountant doing your T2 taxes for you, then once a year they will create a depreciation entry which will lower the amount of your Vehicle Fixed Asset account and increase a Depreciation expense account, the first showing on the Balance Sheet, and the second showing on the P & L.

Again, this is all moot unless you are an incorporated company. Hope this helps!