Solved

Chart of Accounts - Fixed Assets

Hello Community

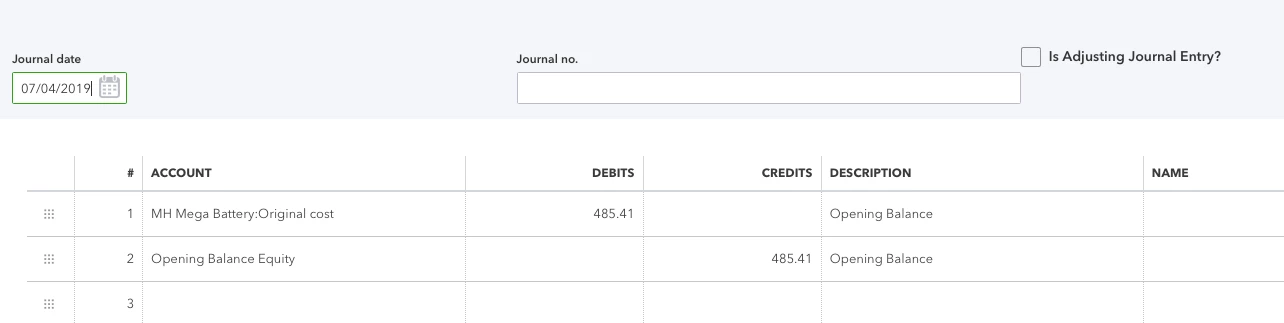

I believe I made an incorrect entry for a fixed asset, I'm trying to correct, and would like to confirm here. I bought a mega battery (expense), when entering the transaction, created a fixed asset category, created subcategory Depreciation, and Original Cost.

The value shown in the name of the asset row appears to double the purchase price. Is this accurate? The images below show my entry. My concern is the value of my asset will not match the tax return. Obviously I'm a little confused at what Quickbooks is doing, and looking for some feedback to help me figure this out.

Thank you

and best regards,

and best regards,