Let's get these balances zeroed out so you can get back to working order, @maryg2.

You'll want to create home currency adjustments to zeroed out the small amounts showing on your balance sheet report. The home currency adjustments change the home currency value of your foreign balances, recalculating them based on a new rate. These adjustments affect your balance sheet accounts.

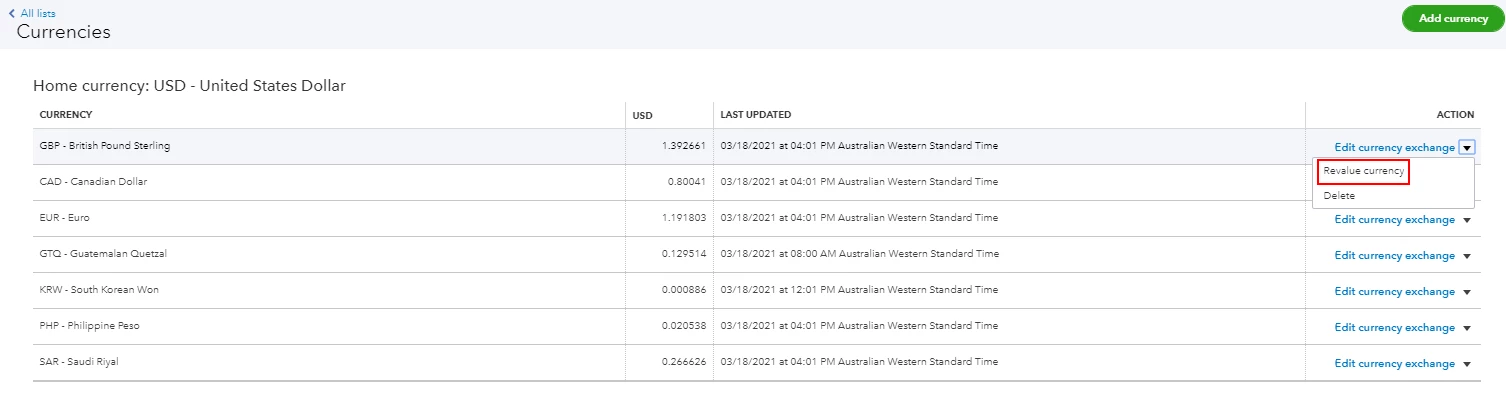

Here's how to create home currency adjustments:

- Click the Gear icon, then select Currencies.

- Locate the currency you want to adjust.

- Under the Action column, select Revalue Currency from the drop-down.

- Select a date (today or a day in the past) to run a currency revaluation.

- Choose whether you'd like the revaluation to be based on the market exchange rate or a rate you specify.

- Select the account(s) you want to apply the revaluation to.

- Click Revalue.

I'm adding this article for more details: Enter home currency adjustments for your foreign balances.

Moving forward, you'll want to perform this every month to make sure the Chart of Accounts (COA) balance and the conversion amount balance on the Balance Sheet will match the actual bank. Not doing this will show a difference in the balances between the Balance Sheet and COA.

You might also want to check out this article to learn more about multi-currency in QuickBooks: Multi-currency FAQ.

Keep in touch if you need any more assistance with this, or there's something else I can do for you. I've got your back. Have a good day.