Solved

Unpaid Invoices Reducing Balance of Operating Account

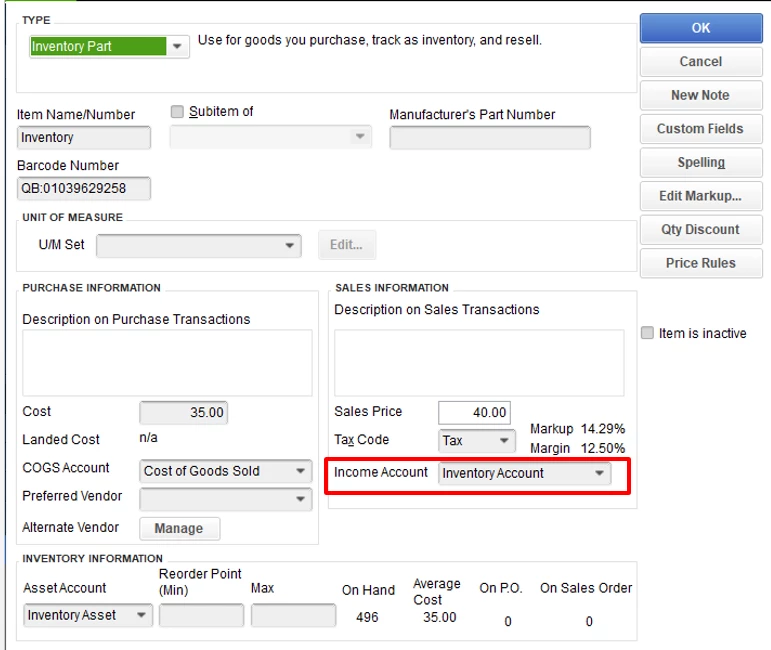

Having trouble understanding our accounts receivables. We invoice a customer for $200, due at some point in the future. Everything appears correct - customer has a $200 outstanding balance in the "customer center", and accounts receivable increases by $200. However, our primary/operating account also goes down by $200 and a new line item (an INV) has appeared in our general ledger as a debit. As a result, our corporate checking account is now $200 less than its actual balance. I do not understand why this debit transaction is being created. Please help. Thanks,